What is an ARM Loan?

An Adjustable-Rate Mortgage (ARM) loan has an interest rate that fluctuates based on a published financial index. The index reflects current market conditions, and as it moves up or down, The Mortgage Office® updates the values and makes them available for download.

What is an ARM Index?

An ARM index is the reference point used to determine the loan’s interest rate.

The Mortgage Office® supports multiple indexes, including:

- 11th District Cost of Funds (COFI)

- CMT (1-Year, 2-Year, 3-Year, 5-Year, 7-Year, 10-Year, 20-Year)

- CMT 3-Month and 6-Month

- Royal Bank of Canada Prime Rate

- Secondary Market CD (1, 3, and 6-Month)

- Secured Overnight Financing Rate (SOFR)

- USD LIBOR – 1 month

- WSJ Prime Rate

CAUTION: Applied Business Software makes every reasonable effort to present complete, accurate information but assumes no liability for errors or omissions.

Each index has different characteristics. For example:

- COFI is a monthly average of interest rates on savings in AZ, CA, and NV.

- CMT indexes are Treasury yields adjusted to constant maturities.

- SOFR measures overnight borrowing collateralized by U.S. Treasuries.

- WSJ Prime Rate is set by a consensus of major U.S. banks.

How to Download ARM Index Rate History

Through the Loan File

- Go to Loan Servicing → Loans → All Loans.

- Select the loan you want to modify.

- Click Edit (pencil icon) or double-click the file.

- Navigate to Terms → ARM tab.

- Click the Index hyperlink.

- Select the index and click Download Latest Rate History.

- In the assistant, check the box for the index(es) you want and click Yes, download index history now.

Through Tasks & Reports

- Go to Loan Servicing → Tasks & Reports.

- Under Adjustable-Rate Mortgages, click Download Index Rate History.

- Use the download assistant to select the index(es) and confirm.

How to Set Up an ARM Loan

TIP: Adjustable-rate mortgages (ARM) are loans where the interest rate changes periodically in relation to an index. Payments may go up or down accordingly.

Steps

- Go to Loan Servicing → Loans → All Loans.

- Select the loan and click Edit.

- In the Terms page, select ARM-Adjustable Rate in the Rate Type dropdown (Options tab).

- Click the ARM tab.

- Choose the Index

- From the dropdown, select the index you want this loan tied to.

- Enter the Look-Back Days

- Specify the number of days prior to the Next Rate Change Date that the system will use to determine the index value.

- Example: With a 45day lookback, if the next rate change is 10/1/2025, the index value as of 8/17/2025 will be used.

- Index (No value needed upon initial setup; this will update once you run your first-rate change.)

- Select the Margin

- Enter the margin to be added to the index to calculate the fully indexed rate.

- Optional Adjustments

- Ceiling (Life Cap): The maximum rate the loan can ever reach.

- Floor: The minimum rate the loan can fall to.

- First Change Cap: Limit on how much the rate can change at the first adjustment.

- Periodic Cap: Limit on subsequent adjustments.

- Rounding Method and Factor: Define how rates should be rounded.

- Carryover: Allows unused increases to carry forward into future adjustments.

- Set the Next Rate Change Date

- Enter the effective date when the next interest rate adjustment should occur.

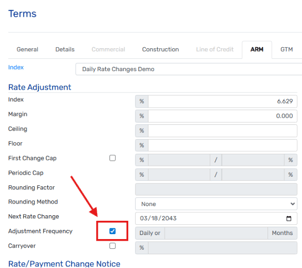

- Select the Adjustment Frequency

- Choose the number of months between adjustments.

- For conventional loans, this is typically monthly.

- For Billable Loans (construction, commercial, line of credit), you can select Monthly or Daily.

- Configure Borrower Notices (Optional)

- Check Send Change Notice if borrowers should be notified of changes.

- Enter Notice Lead Days (commonly 30–45 days before the adjustment).

- Record the First Notice Sent date if applicable.

- Set Up Payment Adjustments (if applicable)

- Check the Payment Adjustment box to enable automatic payment recalculation in the Terms tab.

- Payment Cap, Neg Amort Cap, Recast Payment, Recast Frequency, Recast Next Date, Recast Stop Date, and Recast to Date are all optional fields, depending on loan terms.

- Important: Ensure the Next Adjustment Date is at least one full payment period after the Next Rate Change Date.

- The Adjustment Frequency here typically matches the rate adjustment frequency.

- Option ARM (Optional)

- If the loan is an Option ARM, select the box and configure the available borrower payment options: Interest Only, Fully Amortized, 15-Year Amortized

Key Fields Overview

- Index: Initial rate; updated automatically by the system.

- Margin: Added to the index to establish the fully indexed rate.

- Ceiling (Life Cap): Maximum allowable rate.

- Floor: Minimum allowable rate.

- First Change Cap: Cap on the first adjustment.

- Periodic Cap: Caps on subsequent adjustments.

- Rounding Factor & Method: Define rounding rules.

- Next Rate Change: Date of next adjustment.

- Adjustment Frequency: Months between adjustments.

- Carryover: Carry unused rate increases to future adjustments.

- Payment Adjustments (if applicable): Payment Cap, Negative Amortization Cap, Recast Rules, Option ARM options.

- Borrower Notices: Notice lead days, first notice sent, scheduled rate/payment change settings.

- Look Back Days: The number of days prior to the Next Rate Change Date that the index value is determined. This ensures the correct and available index figure is used for the adjustment.

For example: If the next rate change date is 10/1/2025 with a 45day lookback period, the index value as of 8/17/2025 will be used to calculate the new rate.

TIP: A longer lookback period provides more lead time for preparing borrower notices, while a shorter period uses a more current index value.

Special Considerations for Billable Loans

(Construction, Commercial, Line of Credit)

When dealing with Billable Loans, ARM adjustments work differently:

- Daily Rate Tracking: ARM adjustments are tracked daily, and daily rate changes are automatically created when billing statements are run.

- Payment Adjustment Section Disabled: The Payment Adjustment section is greyed out because TMO automatically recalculates payments during billing.

- Simplified Setup: You only need to configure the ARM tab up to the index and adjustment parameters; payment recalculation is automated.

TIP: Ensure the loan is marked as Billable in setup so that daily rate tracking and auto-payment recalculations are enabled.

How ARM Loans Are Selected for Rate & Payment Adjustments

- Rate Adjustments: Based on look-back days and the next rate change date.

- Payment Adjustments: Based on next adjustment date, notice lead days, and rate change date.

- Combined Adjustments: If rate and payment change at the same time, a single borrower notice is sent.

How to Calculate Rate & Payment Adjustments

- Go to Loan Servicing → Tasks & Reports.

- Under Adjustable-Rate Mortgages, click Calculate Rate & Payment Adjustments.

- Select All Loans or Selected Loans by Account.

- Choose All Indexes or a specific index.

- Optionally, exclude borrowers on hold or filter by categories.

- Review the list of loans; check/uncheck as needed.

- Click Next → Finish.

- If errors occur, review the Errors & Exceptions Report, correct issues, and rerun.

- If successful, TMO confirms that adjustments were added. You can validate by reviewing the ‘Scheduled Rate & Payment Changes’ on the loan file.

How to Edit Borrower Adjustment Notices

- Click the Options.

- Go to Notices → ARM tab.

- Choose the notice type:

- Standard Notice (non-RESPA)

- RESPA Initial Notice (210–240 days before the first change)

- RESPA Regular Notice (60–120 days before subsequent changes)

- Click Download to customize in Microsoft Word (with add-in). Then Upload the newly edited template.

- Save changes or cancel to exit.

ARM Loan FAQs & Servicing Tips

Borrower Notices

- Send notices at least 25 days before the new payment takes effect.

- Must include borrower contact information for inquiries.

Interest Rate & Payment Change Together

- Only one notice is required when both occur at the same time.

Negative Amortization

- If payments don’t cover interest, unpaid interest is added to the principal balance.

Payment Shortages

- Do not automatically reject; apply partial payments where possible and hold unapplied funds until a full installment is available.

Payment Overages

- Handle based on amount and policy.

Nature of Adjustment Errors

- May involve rate, payment, or both.

- Common causes: wrong index, wrong margin, incorrect caps, or failure to apply caps.

✅ You are now equipped to set up and manage ARM loans in The Mortgage Office® — including Billable Loans, borrower notices, rate/payment calculations, and compliance requirements.